Flood Insurance

Opening the Floodgates

As the federal government opens the flood insurance market to private insurers, the industry speaks about the risks, the need for more data and the way forward.

- Best's Review staff

- December 2018

-

Key Points

- Stormy Weather: Hurricanes Harvey and Florence caused historic floods and flooded thousands of homes. Most losses were not insured.

- Market Developments: The federal government has dropped the NFIP’s Write-Your-Own noncompete clause, allowing participating insurers to sell private flood insurance.

- Data Call: Insurers say they need more data about flood risk. Advances in technology will allow insurers and reinsurers to better understand, assess and quantify the risk.

Massive flooding from hurricanes Florence and Harvey resulted in billions of dollars in economic damages. Most of these losses, however, were uninsured.

That's because the private market for flood insurance remains small, and coverage under the federal government's National Flood Insurance Program is limited. Only about 12% of Americans have flood insurance policies, according to a 2016 poll by the Insurance Information Institute.

The private market, however, may start to take on a greater role in covering flood now that the Federal Emergency Management Agency has reduced the National Flood Insurance Program's Write-Your-Own compensation rate and rescinded the WYO non-compete clause. That will allow NFIP participating carriers to sell private flood insurance.

While the NFIP was set to expire on Nov. 30, Congress was expected to extend it.

The federal government has been working to encourage the private market to provide flood cover as it seeks to reduce its own role in this market as the NFIP is about $20 billion in debt to the federal Treasury.

Even so, the private market still often remains on the sidelines.

“As we continue to move forward, the industry will probably be taking up some of the flood insurance programs itself and issuing flood insurance on its own,” said Paul Ehlert, president and chief executive officer of Germania Insurance Co., speaking at the annual conference of the National Association of Mutual Insurance Companies in San Antonio in late September.

“We still need the federal government to get behind and provide actuarial-based rates for the flood program that currently exists,” Ehlert said

The Scope of the Problem

When the skies open, the rain falls and the rivers and streams rise, the damage to property can be extensive. It can be so widespread and so comprehensive, that insurers have for many years considered it an uninsurable risk.

Insurers considered flood a risk that could not be covered because of the catastrophic nature of flooding, the difficulty in calculating rates and the risk of adverse selection, according to a Congressional Research Service report Private Flood Insurance and the National Flood Insurance Program.

“Hurricane Florence in North Carolina this year, like Harvey in Texas [last year], has again exposed the big gap that exists between the economic losses and insured losses, what we call the protection gap,” said Mohit Pande, head of property underwriting for the U.S. and Canada, Swiss Re, speaking at the annual meeting of the Property Casualty Insurers Association of America in Miami in late October.

“Still, one in six homeowners in the U.S. are not insured. There's about 10 billion of economic losses from the peril of flood that goes uninsured each year. NFIP, the government program, is addressing a small portion of it. We feel there's an enormous opportunity for private insurance to address this gap,” Pande said.

Indeed flood was a topic of discussion at the PCIAA annual meeting.

“The undercoverage for flood damage,” said David Sampson, president and CEO, Property Casualty Insurers Association of America, when asked about the key issues at the conference. “Eighty percent of properties in Houston last year, residential and commercial, did not have any flood coverage. We're seeing similar numbers reported by CoreLogic this year for [hurricanes] Florence and now Michael,” Sampson said.

“Clearly the NFIP is not penetrating the market the way it should,” Sampson said. “With the National Flood Insurance Program once again up for reauthorization in the months ahead, we think that we really need to have a discussion about bridging this insurance gap, creating better education among consumers about their own risk profile, and also creating more opportunities for private sector carriers to make flood policies available.”

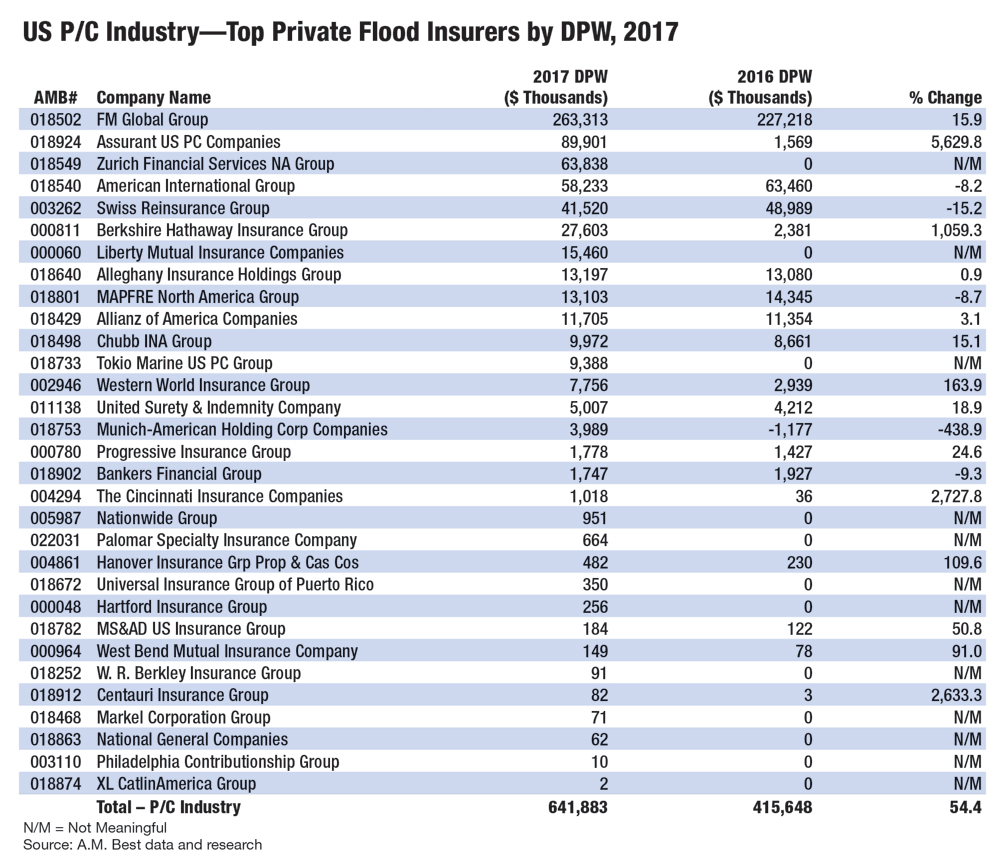

The maximum limit for one- to four-family residential buildings is $250,000; content coverage is limited to $100,000. Private insurers underwrite losses above these limits. In 2017, 31 private flood insurers wrote coverage in the United States, according to the Best's Special Report NFIP Extended but Private Markets May Provide Long-Term Flood Relief.

Susan Molineux

A.M. Best

I think the industry at large is very interested to privatize flood so Americans, and those exposed to flood all over the world, would have access to more coverage.

An Unexpected Market

Many homes and businesses are exposed to flood risk, especially those near coastal areas and near rivers and other bodies of water.

But the risk may be much more widespread than previously understood.

The NFIP has some 5 million policies in force. And it was believed that about 13 million Americans were exposed to a 1-in-100-year flood event, based on FEMA flood maps. A recent U.K. study, however, puts the number of Americans at risk at 41 million.

Approximately 13.3% of the contiguous U.S. is exposed to a 1-in-100-year flood, which translates to a GDP exposure of $2.9 trillion, according to the study from the University of Bristol, Estimates of Present and Future Flood Risk in the Conterminous United States.

The estimate of 41 million people does not include the millions of Americans that are at risk of coastal flooding, the university said.

“It was a little shocking,” Susan Molineux, associate director at A.M. Best said of the study. “Of course, the Bermuda market, and I think the industry at large, is very interested to privatize flood so Americans, and those exposed to flood all over the world, would have access to more coverage.”

Private Hurdles

Shifting coverage from the federal government into the private market, however, has its challenges.

The main deficiency of the NFIP is the program's failure to reflect true risk in premium rates, according to the Best's Special Report.

Subsidized premiums that don't adequately reflect risk exposures, statutory caps on premium increases, the lack of capital requirements or the need to earn a profit and mandatory purchase requirements have all contributed to the program's instability, the report states.

Since 1983, private insurers have been involved in administering the NFIP, including selling and servicing policies and adjusting claims, according to a Congressional Research Service report.

The NFIP retains the financial risk of paying the claims. Private insurers participate in the NFIP in two ways. They can be a direct servicing agent that sells policies on behalf of the NFIP. Or, they participate in the Write Your Own program where they are paid to issue and service the flood policies, according to the Congressional Research Service report.

Some 12% of the total NFIP policy portfolio is managed through the direct servicing agent, and 88% of NFIP policies are sold by the 67 companies participating in the WYO program.

Insurers in the WYO program, however, had to adhere to a noncompete clause issued by FEMA that did not allow them to write their own stand-alone flood insurance policies.

This rule changed in early October. The noncompete clause was removed allowing WYOs to sell primary flood insurance that in the past competed with the NFIP product.

“This change opens the private flood market and provides consumers with a choice of government or private flood insurance and will give them more choices to protect their homes and businesses,” said Don Griffin, vice president of policy, research and international for the Property Casualty Insurers Association.

“More options in the marketplace will be part of the solution to address the major uninsured challenge we face as a nation,” he said.

Some private insurers have already expressed interest in providing flood coverage.

Private insurers have the capital and desire to write flood insurance, according to Kurt Bock, the CEO of Country Financial. Private flood is doable beyond excess and surplus lines, he said.

“We would all like to see the opportunity there,” said Bock, who plans to retire at the end of January.

Asked about growth opportunities, Ed Hochberg, CEO North America, JLT Re, speaking at the PCIAA meeting said, “Flood.”

“The big promise of flood and what will that mean, and just more generally, the hope of business that's in the public sector moving into the private sector and how will that drive growth going forward, I do expect that we will see growth related to those areas in the near future,” he said.

New Tools

Advances in models and other tools may help give insurers more of the information they need to expand their reach in the flood market.

“One of the reasons why we are confident around the insurability of this peril is because of the recent technological advancements that have taken place, which allow us to understand, assess, and quantify this risk,” said Swiss Re's Pande.

But there's still more work to be done, other experts said. To get the private market involved, insurers need more data.

“I think you see massive under-penetration within the flood insurance market,” said Jimmy DeCicco, client manager, RMS.

“The main reason for that, or one of the main reasons, is lack of tools to assess that risk,” DeCicco said. “Flood has always been viewed as a high risk and very difficult to quantify. There's a lot of different sources of flooding, everything from pluvial, fluvial, coastal flooding. You have to account for all of those in a model.

“Until very recently, there haven't been the technological advancements, things like cloud and also the model science, to be able to properly assess those risks and quantify them,” DeCicco said.

“That's changing. There are more and more tools in terms of data models and analytics that are out there on the market to help quantify that risk.

“We're releasing our inland flood model later this fall. We think that with the ability to quantify comes the ability to write that business and expand the market, hopefully grow the flood market and close that gap,” DeCicco said.

Emma Watkins, head of exposure management at The Channel Managing Agency, a Lloyd's managing agency owned by Scor, said private insurers are ready to get involved, but they still need more data.

“We don't necessarily need the data ourselves to underwrite policies, but we need to know that the data is out there and that it's included in the models because we need models, unfortunately,” said Watkins, speaking in May at the RMS Exceedance 2018 conference in Miami.

“We need to be able to understand the risk. We need models and systems that we can rely on and trust in order to price the risk appropriately and be able to carry it,” Watkins said.

Changes at the NFIP and the need for more data were also a big part of the conversation at the RMS Exceedance conference.

“There are a lot of things that FEMA is doing administratively that are helping bring the National Flood Insurance Program to the 21st century,” said Cliff Roberti, managing principal for Federal Hall Policy Advisors. “Through their Risk Rating 2.0 program that's trying to bring more transparency and market information and data to get more accurate rates for policyholders, as well as have them better understand their risk,” Roberti said. “That's currently happening.”

The modeling industry also has a role to play in providing greater insight into the data.

“There's also things that I think we, as a modeling industry, can do to help the policyholder,” said Matthew Nielsen, director of government affairs, RMS. “I say that because I am a policyholder. I know that there are a couple of things that if I'd have known then when I bought my house, I might have thought a little bit differently about my risk.

“Right now, the way that the FEMA maps work you're either in or out of a flood zone,” Nielsen said. “It's very binary. Do you know, in a 1-in-100-year flood zone, are you in a one-foot flood or are you in a 15-foot flood? It turns out where I live, I'm in a 15-foot flood. It would have been nice to know that up front.

“The way that the pricing works in the NFIP is you get one price that is across the entire flood zone,” Nielsen said. “That does two things. One is that people are all in the same flood zone, being charged the same price. There's not an understanding of how severe the flood could be. The second is that there's no real understanding of how much the government is subsidizing the amount of flood insurance that you're paying.

“What that does is it hides the risk that people are bearing when they get their policies,” he said.

Risk Capital

FEMA also has been taking steps to lay some of its risk off into the private market via reinsurance, Federal Hall's Roberti said.

“They did two reinsurance placements, one in 2017 that actually, unfortunately, paid out from the perspective because there were giant storms and people were affected,” Roberti said. “There was a new placement in 2018.”

FEMA also secured $500 million of coverage with a catastrophe bond transaction to provide additional reinsurance for the NFIP.

Combined with the January 2018 traditional reinsurance placement, the August 2018 placement enabled FEMA to transfer $1.96 billion of the NFIP's flood risk for the 2018 hurricane season to the private sector, FEMA said.

FloodSmart Re was the first U.S. flood cat bond and FEMA's first foray into the cat bond market for reinsurance protection for the NFIP flood insurance book, according to Artemis.

A Place for Surplus Lines

Another area for flood coverage comes from the surplus lines market. Surplus lines insurers cover risks that the admitted market won't.

“We're trying to get the admitted carriers a little more comfortable with the peril, [and] let them know that it's a place where they can safely grow some premium,” said Ivan Maddox, executive vice president at Intermap Technologies, speaking at the PCIAA meeting. “We're at that early stage now where things might be making the transition from E&S lines into the more admitted, mainstream insurance markets.”

Surplus lines insurers would be willing and able to increase their exposure to flood risk under conditions that would allow them to underwrite and price risk appropriately, according to the Best's Special Report.

Surplus lines insurers wrote $232.6 million in flood insurance premium in 2017, according to data collected by surplus lines stamping offices for that year. Primary residential coverage accounted for 21.5% of the 2017 total, and 45.3% represented primary commercial.

Surplus lines insurers are looking for legislative clarity that would ameliorate some of the issues that banks have with accepting private flood policies from mortgage holders. Streamlining the process to enter the market will preserve the surplus line industry's ability to provide flood insurance solutions, which could serve as a key component of necessary NFIP reforms, according to the Best's Market Segment Report: Surplus Lines Push Through Various Headwinds for Higher Growth.

Looking ahead five years, Intermap's Maddox says he believes the protection gap will close.

“Ninety percent of the properties that should have flood insurance don't. In five years, if everything goes well, if the admitted carriers are successful, and if we're successful as an analytic provider, those numbers should be flipped,” Maddox said. “We should be talking about, maybe, 5% of the properties in the United States being uncovered for flood.”

While FEMA has taken a number of steps to help shift flood coverage into the private market, the private market now has to step up to the plate, according to E.W. “Ted” Blanch, founder of reinsurance firm Coin Re.

“There's a lot of conversations about flood, flood, flood,” Blanch said at the PCIAA conference.

“My observation is there's more talk than actual action. To the extent we get the flood insurance issue under control, I think if the insurance companies stop talking and start acting we'd get there much quicker.”

Best’s Review editor Lynna Goch and senior associate editors Lori Chordas, Meg Green and John Weber contributed to this report. Best’s Review staff can be reached at bestreviewcomment@ambest.com.