Insurtech: Investing

Proof of Concept

Later-stage insurtech investing increases as incumbents seek partners and results.

Key Points

- Greater Focus: Incumbents have become more strategic in their insurtech investments.

- Partner Search: Carriers and corporate venture capitalists look to invest in partnership-ready startups.

- Pause in Market: The number of insurtech startup launches has declined the past two years.

Insurtech is catching its breath.

After running full sprint for the past five years, the market paused a bit in 2018. The number of new startups decreased, and investors reassessed their portfolios to determine where to make their next bets.

As the insurtech space has matured and investors have grown wiser, carriers have shifted gears in their support efforts. Incumbents—more than two-thirds of whom have or plan to create venture capital funds, according to KPMG—increasingly are investing at later stages, and they are becoming much more strategic with their investments.

“Initially, you saw this wave of new startups coming in, and people spreading their money throughout the industry, trying to figure out who's going to get off the ground fastest,” Sam Friedman, insurance research leader for Deloitte Center for Financial Services, said. “Now, it's a much more discerning investor, I think.

“It's at the point now where you can't just come in with a PowerPoint. You have to be a more mature insurtech. By mature, I might mean 18 to 36 months in operation. They're toddlers. But they're walking, at least, as opposed to still being in the crib, or in the incubator.”

Carriers and corporate venture capitalists (CVCs) have gained a better understanding of emerging technology and its use cases. And, given the abundance of new insurtechs that have launched in recent years, they also now have plenty of startups to choose from.

Experts estimate there are roughly 1,500 insurtech startups, and more than half of them were formed in one five-year period. Between 2012 and 2016, 743 insurtech startups launched, according to data from Venture Scanner.

“There are investors who really know what to invest in, and there is more choice for them to invest in,” Andrew Johnston, global head of insurtech for Willis Re, said. “Back in 2012 and 2013, the number of insurtechs you could invest in was limited, let alone the number of mature insurtechs. Whereas now you have a huge option and you can hedge your bets a bit and wait, and you can see what the market is really doing.

“And I think that's exactly what people are doing. They're reducing their risk by waiting. The trade-off for that is that they're having to invest more money, but there seems to be no shortage of available investment capital at the moment.”

The seed-stage round is just testing. It’s research and development, which the industry doesn’t do well.

Mark Purowitz

Deloitte Consulting

Business Ready

There's still plenty of capital flowing into insurtech. According to Deloitte, insurtech funding was on track to reach nearly $2 billion in 2018. So the money is available; it's just being distributed differently.

That shift began just over a year ago. In the fourth quarter of 2017, Seed and Series A transactions dropped significantly. Whereas those stages have accounted for 65% of all transactions since 2012, according to Willis Towers Watson, they accounted for just 51% of transactions in the fourth quarter.

On the heels of that, in the first half of 2018, late-stage investments climbed to 46% of transactions, according to Deloitte. It marked a significant jump from the five previous years. Between 2013 and 2017, late stage-investments, defined as Series C and beyond, comprised 37% of total transactions.

Mark Purowitz, global insurtech leader for Deloitte Consulting, said the move toward later investments is due to maturity.

“The investment community learned that funding ideas from PowerPoint slides wasn't the greatest way to go about it. A lot of companies in the past got funding for ideas,” Purowitz said. “What we are now seeing is a more evolutionary, more mature mechanism. They want to see a more thoughtful approach—not only about the market and the opportunity, but the solution. They want something more demonstrable.

“These early-stage companies are actually too immature and too early for the carriers to consume them in their operating model constructs,” Purowitz added.

That notion of adoptability is key. Increasingly, insurers are looking to increase investment in startups that are partnership-ready.

Ted Stuckey, managing director at QBE Ventures, said his team actively seeks companies whose products can be incorporated into the parent company.

“We're very focused on the partnership angle,” Stuckey said. “Before we invest we want to see a strong possibility that we can leverage the product within QBE in the near term. We don't have a ton of preference about being the first customer or the 15th customer. What we're hyper focused on is: Can this move the needle for QBE now?”

Jennifer Byrne, the co-founder and president of innovation consulting firm Quesnay, said carriers are pressed to move that needle.

“There is a demand for incumbents to meet the needs of their customers, whether through their digital experience or more customized products,” Byrne said. “Insurtechs have developed relevant solutions and can look at the problems in a way that incumbents haven't been able to and at a faster pace. Incumbents have a lot of value to provide as well, their data and customer base, in particular, are why many insurtechs are looking to partner rather than to disrupt—something that isn't as common in other industries.”

Investing in partnership-ready startups is not just a good business decision, Stuckey said. It's also a good investing decision.

“We believe that if we can be a customer of our portfolio companies, then there is something about them that is going to mean other carriers would be a customer as well,” he said. “It's not easy to work with large insurance carriers. So the fact that we can work with them means that they have a product that is solving for a real need, is providing real value and should ultimately be a meaningful lever in a carrier's transformation.

“That makes it a really good investment.”

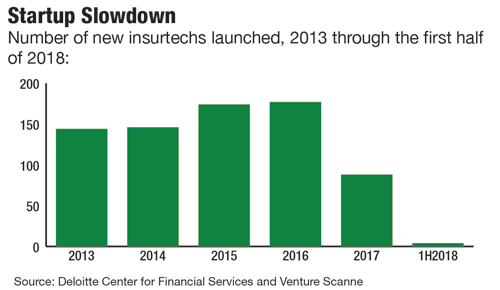

Startup Slowdown

The slowdown in new insurtechs—and maturation of existing ones—also factors into current investing trends.

There are simply fewer new insurtech companies being formed. After averaging 160 launches per year from 2013 through 2016, the number of new startups dropped to 88 in 2017 and came to a near standstill in the first half of 2018. Only four insurtechs launched in the first six months of last year, according to Venture Scanner.

“The slowdown is a natural sorting of where these businesses are being funded, how they're being funded, and what the growth prospects are for them,” said Doug Russell, managing director and head of MassMutual Ventures. “Broadly speaking, though, I think it's just a pause.”

As is typical with startup cycles, insurtech now has reached a copycat phase, which experts say has led to a reduction in quality.

“We're starting to see carbon copy companies, which obviously aren't going to attract the same level of early-stage investment,” Johnston said. “And as the number of new startups increases, the quality diminishes. That's not surprising. We have observed some insurtechs that have been rushed into 'market readiness' without a proven thesis-driven approach to the industry.

“So people are able to wait a little more. They're not under pressure to invest.”

Waiting has its benefits. Many startups pivot during their early days, changing course as they mature. Slice, for instance, started as a digital platform providing episodic insurance for the sharing economy. Now it offers its operating system to insurers as digital insurance as a service.

“We're seeing a shift in the landscape of the early stages of insurtechs as they better understand the marketplace, as they better understand where and how they fit in, as they better understand where and how carriers can consume what it is that they're offering,” Purowitz said.

“The seed-stage round is just testing. It's research and development, which the industry doesn't do well,” Purowitz added. “Once you've gotten through the early stages of R&D, you get a greater sense of clarity around what you're solving for.”

Investing during those early-stage rounds is riskier.

“Most of the CVCs are looking for strategic investments,” Johnston said. “They are typically less risky in their investments, whereas in the traditional VC and PE [private equity] world, they work on a numbers rule rather than an industry or track record rule.”

Carriers and CVCs want, and in many cases need, to see a track record.

“Early on there was a lot of blue sky work being done. They were throwing money at people and seeing what they come up with,” Friedman said. “Now there's much more of a demand for quantifiable results. Show me progress.

“So that also argues for the later stage, because they have a track record. They've either met deadlines or they haven't. They have a prototype or a model that's being beta tested.”

The CVCs, too, need to show results—to their own companies.

“They've been around the track a few times,” Friedman said. “They've been to show-and-tells. They've worked with accelerators. They've done 'Shark Tank' exercises. They've gone through these preliminary exercises to get a sense of what's out there. And they've made some bets. Now they want to show their people results.

“There are more demands being made all around, which is why people are going for later stages.”