Startups: Commercial Lines

Taking Care of Business

Insurtechs look to ease pain points in commercial lines.

SMALL BUSINESS ROW: In the U.S., 82% of small-business insurance buyers bind through the agency channel. As a result, many insurtechs are trying to support the channel rather than compete with it.

Key Points

- Big Business: Small business is big business, with a market size in the range of $100 billion.

- Helping Hand: Nearly two-thirds (63%) of commercial lines insurtechs are looking to enable the existing value chain.

- Pain Points: Insurtechs largely focus on digital interaction and core insurance capabilities, looking to improve customer experience and profitability.

Three of the four insurtech startups Matt Streisfeld has invested in are focused on commercial insurance. It's a space the Oak HC/FT principal loves, largely because of its abundance of problems.

“There are so many pain points,” Streisfeld said. “And there is so much fat in the supply chain that can be absolved with streamlining the process.”

The insurtech community appears to feel the same. While the early wave of insurtechs targeted personal lines, more and more are setting their sights on commercial lines. According to McKinsey, 39% of today's insurtechs work in commercial lines, and the majority of those are focused on small business.

It's easy to understand why. The small-commercial market is large, fragmented and inefficient. Yet it's also profitable, with businessowners policy loss ratios holding around 65% in 2017, according to Verisk.

Depending on how it's defined, the small-commercial segment has a value of anywhere from $90 billion to $135 billion. And according to Accenture, no single carrier has more than 4% market share in small commercial, which creates opportunity for market share growth.

In addition to those economic factors—which of themselves make commercial lines attractive—the space also is highly inefficient. With its cumbersome questionnaires, slow pace and high operational costs, commercial lines insurance, particularly small commercial, is friction-filled.

Combined, these elements make small commercial alluring to both incumbents and newcomers.

“It is very attractive to not only insurtech startups, but also the insurance industry as a whole,” said Scott Ham, CEO of digital small-commercial insurance solutions for McKinsey.

On the incumbent side, there are plenty of examples of carriers looking to expand or improve their reach into the small-business market. Travelers acquired Simply Business, a U.K. small-to-medium-size enterprise insurance broker, in an effort to expand its small-business presence. Allstate launched an insurance quoting platform for small business. Starr has a unit, Starr Insure, that sells directly to small businesses. The list goes on.

Carriers equally are looking to insurtechs for help in better reaching and servicing the small-business market. Small-commercial insurtechs can be found all along the value chain, from customer acquisition through claims handling. And unlike many of their personal lines predecessors, most small-commercial insurtechs have positioned themselves as enablers of the value chain rather than disruptors of it.

“I never use the word disruption,” said Allan Egbert, co-founder of Ask Kodiak, a platform that allows P/C carriers to share their risk appetite with agents and brokers. “We don't think in terms of disruption or breaking the mold. For us, our focus is primarily on customers and building companies.”

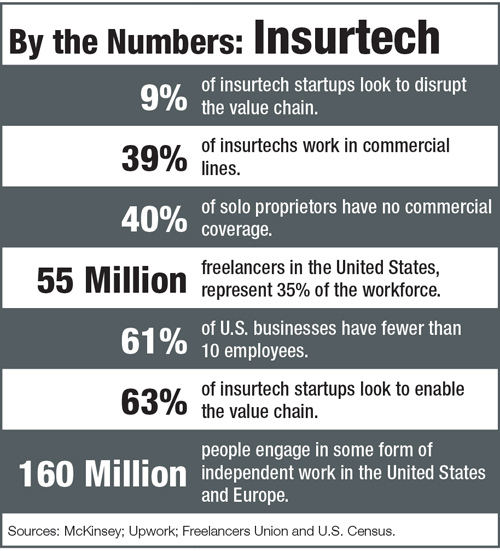

A mere 9% of commercial insurtechs are looking to disrupt the full value chain, whereas nearly two-thirds (63%) aim to enable it, according to McKinsey.

Ryan Hanley, chief marketing officer of Bold Penguin, understands that rationale. While he sees plenty of room for improvement in the small-commercial space, he sees no need for full scale disruption.

“Disruption is the wrong goal,” said Hanley, whose company built a platform that connects businesses, agents and carriers. “It's a great buzzword. It gets you press. It gets people writing about you, looking at you. Tech Crunch or The Verge will write an article about you if you plaster 'disruption' all over. But disruption is not actually a fruitful endeavor because our industry works incredibly well.

“There are just points in the value chain where there is intense friction—problem-causing, issue-driving friction.”

Increasing Efficiency

The small-commercial space offers growth potential on several fronts. Not only is it fragmented, which means market share gains are up for grabs, but McKinsey reports that 40% of solo proprietors have no commercial coverage. That's a lot of underinsured people.

According to research by Upwork and the Freelancers Union, there are 55 million freelancers in the United States, which translates to 35% of the workforce. In the United States and Europe combined, more than 160 million people engage in some form of independent work, according to McKinsey.

Insurtechs such as Dinghy and Zego have targeted these untapped pools. Dinghy, which in January was acquired by U.K. insurer Kingsbridge, provides flexible insurance for freelancers through a mobile app. Zego, meanwhile, provides on-demand insurance for gig economy workers.

But more often than not, insurtechs are looking to address pain points in the traditional small-business insurance process. With the segment still relying heavily on human judgment and manual processing, inefficiency is one of the biggest pain points.

“You have a high-cost, high-touch model, which means there's a lot of human interaction, a lot of human judgment involved in commercial and small-commercial business,” Ham said. “You also have an agent experience or a consumer experience, when talking about the buying or selling experience, that is not intuitive. It's a bit clunky and burdensome in terms of the number of questions that are asked and the amount of information that's requested. Finally, you have a time period of weeks to go from application to delivery and binding.”

Insurtechs are addressing all of those problems, but Ham said they are particularly focused on two areas—digital interaction and core insurance capabilities.

“They're trying to build more intuitive platforms with fewer questions,” Ham said. “They're also working on straight-through underwriting so that a human doesn't have to touch the simple cases. The same with claims. Those are the big areas insurtechs are focusing on now.”

On the operational side, insurtechs are looking to drive costs out of the business. How they do so varies. Shift Technology, for instance, uses technology to reduce fraud. Risk Genius uses artificial intelligence to streamline policy language and create more efficient workflows. Hyper Science automates data entry by making content machine-readable.

On the digital interaction front, companies such as Next, CoverWallet and Insureon use artificial intelligence and machine learning to speed up the process and enhance the customer experience. Insureon, which has sold more than 200,000 policies, targets businesses with fewer than 10 employees. According to U.S. Census statistics, 61% of all businesses fit that size category.

“They are targeting micro businesses and providing them with vertically focused insurance products, providing them with price shopping to a degree,” said Streisfeld, who counts Insureon among his investments. “They take an Amazon approach, or a personal lines approach, to the commercial world. And it works with that type of customer.”

Steve Tunstall, CEO of Inzsure, takes a similar approach at his Singapore-based startup. Inzsure's platform allows small-and-medium enterprises to compare and buy insurance, with Inzsure providing end-to-end customer support throughout the process.

“Whilst much of the industry has an inward, product focus, Inzsure is more about finding what the customer needs amongst the often confusing and jargon-riddled insurance landscape,” said Tunstall, whose company received a broking license from the Monetary Authority of Singapore. “By simplifying the onboarding process, Inzsure makes it easier for decision-makers to get a good sense of what they need. Insurance remains a complex solution to difficult risks. Over-simplification is as problematic for the customer long term, as is confusion from the complexity. It's challenging to tread the right line.”

You have a high-cost, high-touch model, which means there’s a lot of human interaction, a lot of human judgment involved in commercial and small-commercial business.

Scott Ham

McKinsey

Assisting Agents

Particularly outside the United States, agents are viewed as highly susceptible to disintermediation by insurtechs. Tunstall said small-business insurance buyers in Asia distrust the industry and have been poorly served by agents.

“There is an old adage that insurance gets sold, it doesn't get bought,” he said. “Over the years this has been the task of intermediaries?—agents and brokers—who communicate directly with customers and explain why insurance is a good thing. When it works well, it's a tremendous partnership. When it doesn't work well, the customer feels they are getting poor or biased advice. As with many intermediary processes, there is little transparency as to who is really working for whom.”

Tunstall noted the U.S. market is different, saying the traditional model is entrenched there “because there - is - no - choice.”

In the United States, 82% of small-business insurance shoppers bind through the agency channel, according to McKinsey. As a result, many insurtechs are trying to support the channel rather than compete with it.

Xagent, for instance, offers a single-entry market access solution for property/casualty agents, allowing agents to obtain multiple quotes at one time. In addition to its direct-to-consumer platform, CoverWallet also has a platform for agencies. Indio, meanwhile, offers a management platform for commercial insurance brokers. And Bold Penguin helps agents find, quote and bind more policies in less time.

The efficiencies that these startups offer are particularly important for small-commercial agents, who make small commissions on these policies, even though they require more attention. By eliminating some of the “touch” from this high-touch model, the margins can grow.

“Small commercial is incredibly profitable, or it can be profitable for carriers,” Hanley said. “Today, it is very difficult to be profitable as a broker or an agent in small commercial.”

Increasing profitability and improving efficiency are the goals of insurtechs like Bold Penguin, which still believes firmly in the human agent for commercial lines.

“If we look at the whole process and we say, 'It's broke,' that's the wrong language,” Hanley said. “Language matters when we have these discussions. The process is not broke. There are pieces of the process that we need to specifically address.

“If we can help reduce the friction points, then we've given this industry's strongest assets, its human beings, the tools they need to be value providers in the moment when that customer needs them.”