Risk: Litigation

Legal Maneuvers

Casualty insurers try to catch up to a shifting litigation landscape. Special Risk Section sponsored by LexisNexis.

Key Points

- Inflated Risk: Litigation risk has grown in response to shifting jury demographics, anti-corporate sentiments and the rise of litigation funding firms.

- Plaintiff Pool: Both the number and types of plaintiffs are expanding.

- Rate Reaction: Casualty insurers are raising premiums to catch up with increased loss costs stemming from market dynamics.

Stephen Catlin has been sounding the alarm, warning that casualty insurers face a crisis of catastrophic proportions.

A decade of underpricing has left the industry ill-prepared to handle the growing exposure created by social inflation and inflated jury awards, the founder of Convex Group wrote in February's Best's Review.

Social inflation has become a scourge on the industry. Some argue the industry brought the crisis on itself through inadequate pricing and reserving, but there is no question that the litigation landscape has shifted.

The term “social inflation” generally describes societal trends that have contributed to the increasing costs of liability claims. That catch-all descriptor, however, boils down to some very concrete changes affecting litigation.

Those changes have caught some casualty insurers off-guard.

Observers point to an expanding pool of plaintiffs, shifting jury demographics, negative public attitudes toward corporations and the rise of litigation funding firms as factors amplifying litigation risk in liability lines.

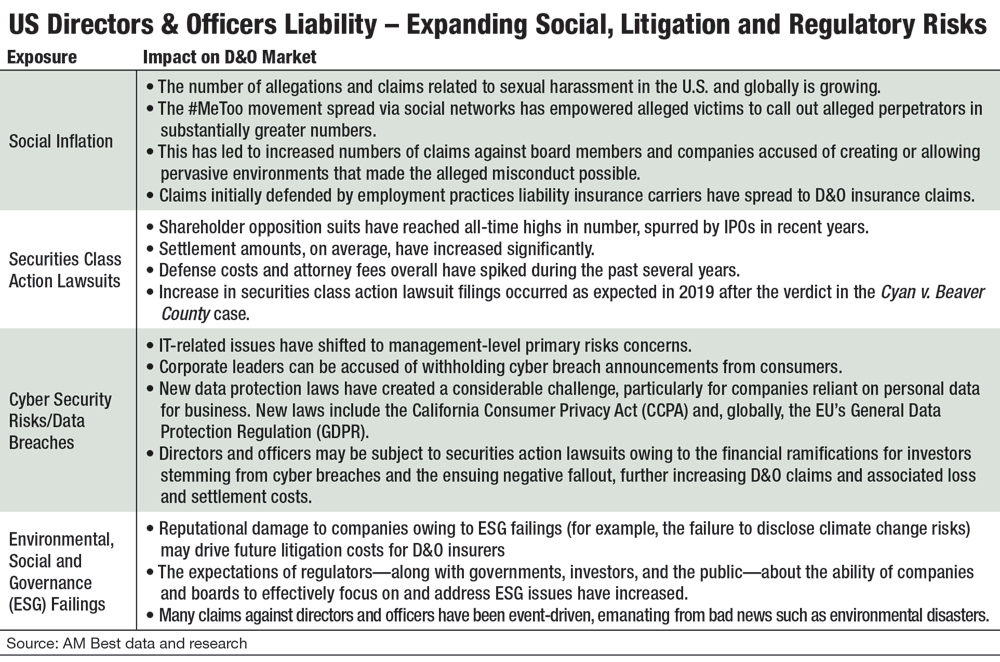

Contributing to the problem is that the same claims are hitting multiple lines, so insurers are defending them repeatedly. Claims of workplace harassment, for example, once principally defended under employment practices liability policies, are seeping into the directors and officers line.

Carriers also are seeing a spike in securities class action lawsuits following the Supreme Court's Cyan v. Beaver County Employees Retirement Fund decision. And they are defending against new legal theories seeking nontraditional damages.

All of these factors have increased systemic risk.

“The exposure has been amplified,” Sridhar Manyem, director, industry research, AM Best Rating Services, said.

Market conditions underlying these litigation trends are unlikely to change. Rates, therefore, must. At the PLUS D&O Symposium in February, insurers called today's loss environment “the new normal” and said premiums must reflect the reality of the exposure.

“The heightened level of litigation, that's not going to change,” Danny Hojnowski, executive vice president of TransRe, said at the symposium. “We all talk about the #MeToo movement, event-driven litigation, litigation financing, there's so many different things—buzzwords—that keep being talked about at all these conferences. For me, the biggest challenge facing the industry is complacency on the part of underwriters.

“In the past year we were able to achieve about 20% rate across multiple management liability lines of business,” Hojnowski said. “That's good, it's not great. We need to keep pushing double-digit rate increases as an industry.”

New Pools

Opioid litigation provides a prime example of the expanding plaintiffs' pool. Many of the largest suits were filed by communities seeking recompense for financial damages caused by addiction.

“If you look at the opioid litigation, the plaintiffs are a lot different than in previous litigation that was like opioids,” Bob Reville, CEO of Praedicat, said. “Opioids is part of a longer line of litigation that goes back to tobacco. In the tobacco litigation, you had only states who were the plaintiffs and only six tobacco companies that were the defendants. That resulted in a $250 billion settlement to be paid out over 25 years.

“In years after that, one thing that emerges is that other levels of local government that have faced expenses from tobacco public health issues have not had access to the tobacco settlement fund. With the opioids litigation, you have not just states involved in litigation, but local governments, tribal nations and even recently, school districts. What that means is you have a lot more plaintiffs and more types of damages that are being claimed in the litigation.”

In October, two Ohio counties reached a $260 million settlement agreement with three drug distributors and an opioids manufacturer. That same month, the Miami-Dade School District in Florida sued a dozen opioids manufacturers and distributors to recover costs it has incurred as a result of the opioids crisis, including money spent training school nurses on how to treat an overdose, providing mental health counseling for students affected by the epidemic and hiring additional security to prevent opioids from entering the schools.

Reville warned that similar suits could arise from other issues, such as exposure to Roundup Weed Killer, diesel exhaust or even sugar.

“It's not hard to imagine that this could be a model for other litigation,” Reville said.

Michael Menapace, an attorney with Wiggin and Dana, said the expanding range of plaintiffs has caught some off guard.

“It's fair to say that insurers expect that when companies manufacture and sell products there will be a certain number of claims associated with those products. That's part of the industry,” Menapace said. “I would doubt that many people expected this new wave of types of plaintiffs.”

Menapace added that corporate plaintiffs, such as self-funded health plans and multiple employer welfare arrangements, are also bringing class or mass actions against pharmaceutical companies for alleged misrepresentations in sales and marketing. Such suits illustrate a change in legal theory, particularly as applied to commercial general liability insurance.

“It's not, 'I took this bad medicine and now I'm suing you for bodily injury,'” Menapace said. “The theory is, 'We spent more money on this than we should have, and we're injured financially.

“So we have insurers who have issued CGL policies, and we no longer just have plaintiffs who are claiming bodily damage, which is one of the two triggers for a CGL policy. Is the CGL policy duty to defend even triggered when you're defending against somebody who's claiming only monetary loss? The courts are wrestling this, and different courts have gone different ways.”

To a carrier, the demarcation line in such situations might seem clear. But this is where social inflation comes in. Shifting jury demographics and anti-corporate sentiment can impact contract interpretations.

“There could be a liberal interpretation of a contract or you could have a really strict interpretation of a contract,” Manyem said. “The way the contracts are being interpreted is becoming more plaintiff friendly.”

Jury demographics, particularly the emergence of millennials in jury pools, have contributed to this shift. According to the 2019 Deloitte Global Millennial Survey, only 55% of millennials view business as having a positive effect on society and 26% of millennials said they do not trust business leaders as sources of accurate information.

“You're seeing more plaintiff-friendly juries and courts, and increased penalties,” Manyem said.

The way that actuaries react to these trends is very important. You need to make sure you set reserves appropriately.

Sridhar Manyem

AM Best Rating Services

More Suits

Perhaps not surprisingly, D&O lines are being hit particularly hard as a result of changing sentiments toward corporations. According to the Best's Market Segment Report Expanding Risk Exposures Present D&O Insurers with Significant New Challenges, professional liability insurers are facing a “minefield of potential litigation” and defense and cost containment expenses in 2018 were 57 percent higher than in 2011.

In the wake of the #MeToo movement, boards are being accused of creating environments that have allowed for sexual harassment to occur. They're also frequently targeted by shareholders over the financial impact of cybersecurity breaches and environmental, social and governance (ESG) failings.

“It seems like nowadays everything is [deemed] securities fraud,” Hojnowski said. “If you have any sort of stock drop, you're going to be sued.”

Many suits revolve around disclosures. For example, Exxon Mobil was sued in November for allegedly misleading investors about the risk of climate change on its business. In the case of data breaches, Manyem said, boards are being sued for not disclosing breaches quickly enough and for failing to adequately protect information.

“The disclosures become really important,” Manyem said. “Plaintiffs say, 'You, directors and officers, stated in your 10-K that you look at employment practices regularly. But you didn't fulfill it appropriately. Or you said the company takes all methods to ensure that data is protected. That disclosure is wrong because you just got breached. How did you ensure this didn't happen? Why did you tell us that you ensured it?'”

Shareholder opposition to IPOs and mergers and acquisitions also is on the rise, with securities class action lawsuits at an all-time high. According to Cornerstone Research, a record 428 federal securities class action lawsuits were filed in 2019, spurred by 2018's Cyan verdict, which allows plaintiffs to file in both state and federal courts as opposed to just federal court.

Cornerstone reported that the number of filings in state courts rose to 49 in 2019, a 40% increase from the previous year. Almost half of those, it said, had parallel actions in federal court.

“That's played an important part in D&O in terms of the increase in frequency,” Manyem said. “Earlier there was just one court where litigants could go whereas now they can file in multiple places.”

Class action litigation, whether related to securities or related to products such as Roundup, is often supported by litigation funding firms. These firms provide financial resources for plaintiffs to bring suit. This type of funding is considered a new global investment class and attracts investors seeking higher returns.

“There are very well capitalized litigation funding firms that use sophisticated financial modeling to decide what suits to bring,” Menapace said. “Not a week goes by where I don't get an email from a litigation funding company asking if I want to talk about my current cases and whether they can assist. They don't realize I don't do plaintiffs work; they're just blasting all lawyers.”

New Normal

Insurers can't control many of the dynamics impacting casualty lines. But experts say they can improve underwriting, pricing and communication between their actuarial, underwriting and claims departments.

“Insurers sometimes miss the boat on trends,” Manyem said. “The way that actuaries react to these trends is very important. You need to make sure you set reserves appropriately, and you have certain inflation assumptions that you take into account in doing so. When those inflation assumptions change, actuaries need to react appropriately and claims people need to communicate with their underwriters so the underwriters can factor it into pricing. The communication loop, in terms of risk management, becomes very important.”

Pricing also is critical. After years of declining pricing, rates increased almost across the board in casualty lines in 2019. According to the Council of Insurance Agents &Brokers, commercial lines premiums went up every quarter in 2019. D&O rates increased by as much as 32% in the fourth quarter, while employment practices liability increases were as high as 22%.

Hojnowski said the D&O market is correcting itself. The problem and solution facing D&O lines, he said, can be explained with simple math.

“There are two components to a loss ratio, you have premium and then you have losses,” Hojnowski said. “On the premium side, if someone started out with a 60% loss ratio, which is where much of the industry thought that the D&O books were running to, [and] you give back 5% in premium over five consecutive years, your loss ratio just ballooned to a 77. This doesn't take into account any sort of claim inflation that we've heard so much about.

”On the claims side, take a similar scenario. A 60% loss ratio in 2012. Now if you add just a simple 5% claim inflation number to that, and you fast forward seven years, you're now at an 84. When you combine those two factors, you're well over 100 loss ratio, and that's a 100 loss ratio, not combined ratio. I call it a correcting market, because the market clearly needed rate, and we saw that come in in 2019.”

Bethany Greenwood, head of executive risk for Beazley, agrees this is a correction.

“I've been asked about how long this might last,” Greenwood said at the PLUS D&O Symposium. “I think that it is a bit of the new normal, because what we've seen in the legal environment has actually only deteriorated from when we put those policies in place three years ago. Litigation's going up, frequency is up, severity is up, so it just lends itself to premium being up.”

Kate Smith is managing editor of Best’s Review. She can be reached at kate.smith@ambest.com.

Meg Green, senior associate editor, AMBestTV, contributed to this story.